Which of the Following Circumstances Creates a Future Taxable Amount

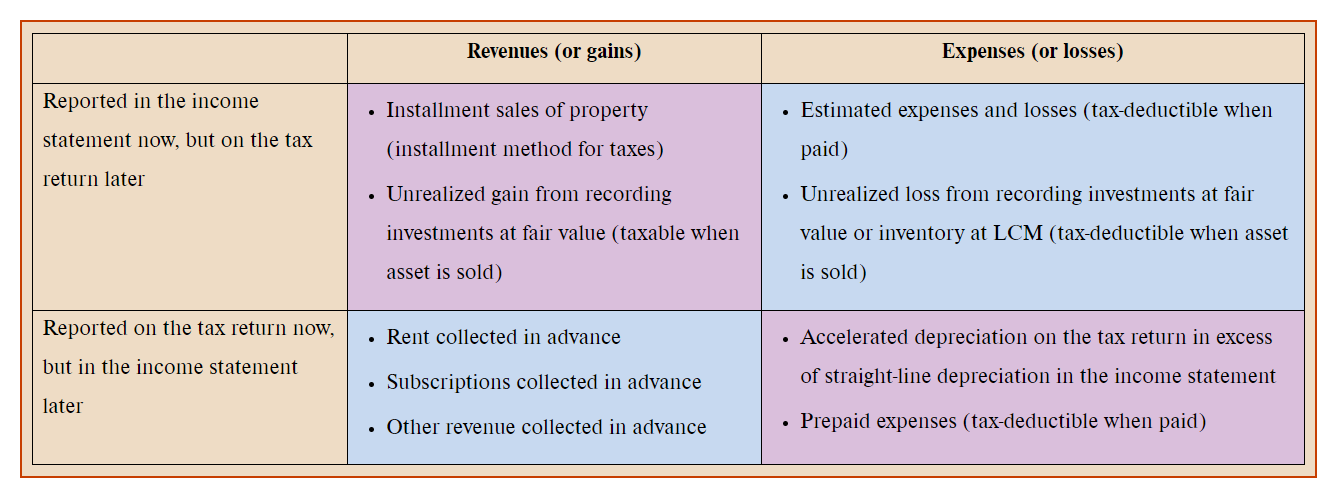

Taxable when received recognized for financial reporting when earned. Straight-line depreciation for financial reporting and accelerated depreciation for tax reporting.

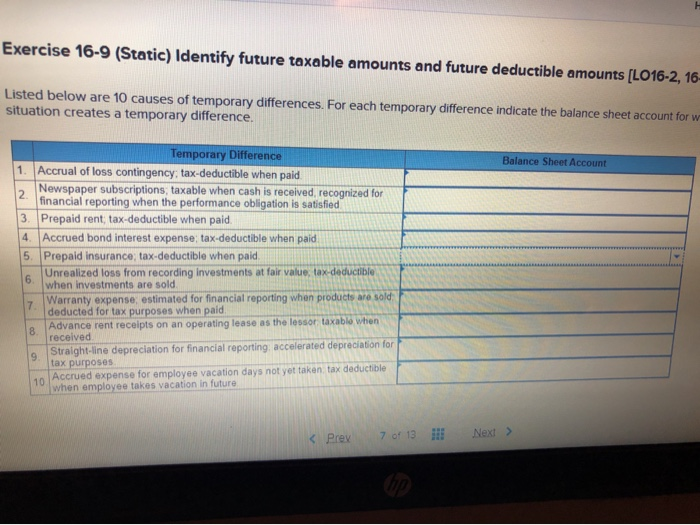

Solved Exercise 16 9 Static Identify Future Taxable Chegg Com

Straight-line depreciation for financial reporting and accelerated depreciation for tax reporting.

. Taxable when received recognized for financial reporting when earned. Component of stockholders equity. Straight-line depreciation for financial reporting and accelerated depreciation for tax reporting.

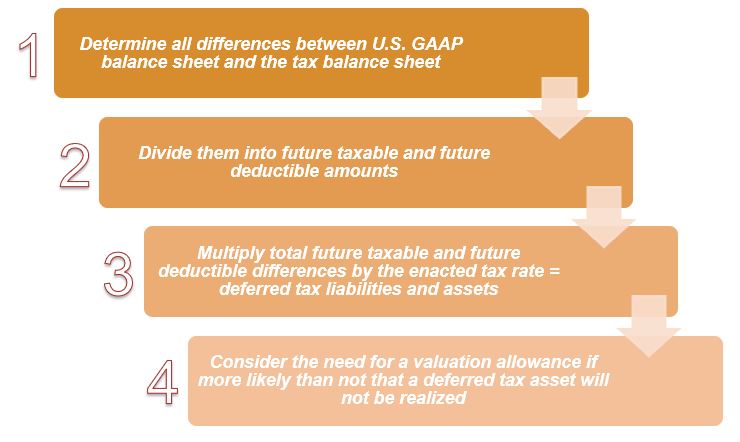

Taxable when received recognized for. Each years tax expense on the income statement includes the current portion related to tax payable in the current year and the deferred portion that includes any changes in deferred tax assets and liabilities. Which of the following circumstances creates a future deductible amount.

For married filing separate returns the amount is increased to 5250 previously 2500. For 2021 the amount is increased to 10500 previously 5000. Accrued compensation costs bonuses paid in the future.

Which of the following circumstances creates a future taxable amount. Accrued warranty expenses. Which of the following circumstances creates a future taxable amount.

Which of the following circumstances creates a future taxable amount. In future years tax depreciation will be less than financial. Answer d is a permanent difference that.

Service fees collected in advance from customers. Accrued compensation costs for future payments. Straight-line depreciation for financial reporting and accelerated depreciation for tax reporting.

Interest received on municipal bonds. Taxable when received recognized for financial reporting when earned. Operating loss carryforward Will always create a deferred tax asset.

O Rent collected in advance. Which of the following circumstances creates a future taxable amount. Taxable when received recognized for financial reporting when earned.

Accounting depreciation meaning future taxable income. One results in a future taxable amount such as revenue earned for financial accounting purposes but deferred for tax accounting purposes. Service fees collected in advance from customers.

Taxable when received recognized for financial reporting when earned. Is the process of allocating income taxes among two or more reporting periods by Prior period adjustment Would be either debited or credited to retained earnings net of any tax effect. The second type of temporary difference is a future deductible amount.

Accrued compensation costs for future payments. Yes Yes 33 15. Which of the following creates a deferred tax asset.

Sales of property installment method for tax purposes. Which of the following creates a permanent difference between financial income and taxable income. Which of the following usually results in an increase in a deferred tax liability Prepaid operating expenses currently deductible.

Service fees collected in advance from customers. Which of the following circumstances creates a future taxable amount. Accrued compensation costs for future payments.

Future Future Taxable Amounts Deductible Amounts a. Service fees collected in advance from customers. Multiple Choice 0 An unrealized gain from recording investments at fair value.

Service fees collected in advance from customers. Multiple Choice Service fees collected in advance from customers. In order to determine taxable income each January the EDD sends a Form 1099-G to each individual for the total unemployment insurance benefits paid during the prior year.

Service fees collected in advance from customers. Accrued compensation costs for future payments. Differences between the carrying.

Which of the following circumstances creates a future taxable amount. Taxable when received recognized for. This may happen if a company uses the cash method for tax preparation.

Which of the following circumstances creates a future taxable amount. Service fees collected in advance from customers. The principal issue in accounting for income taxes is how to account for the current and future tax consequences of the following.

Service fees collected in advance from customers. Accrued compensation costs for future payments. Earning of non-taxable interest on municipal bonds.

Accelerated depreciation in the tax return. Accrued compensation costs for future payments. If you dont receive your Form 1099-G by mid-February you may call.

The future tax consequence of temporary differences will be to increase taxable income relative to accounting income. Deferred tax liability Arises when future taxable amounts are created by temporary differences. Taxable when received recognized for financial reporting when earned.

See the answer Show transcribed image text Expert Answer 100 7 ratings. Will exceed future financial accounting income. IAS 12 implements a so-called comprehensive balance sheet method of accounting for income taxes which recognises both the current tax consequences of transactions and events and the future tax consequences of the future recovery or settlement of the carrying amount of an entitys assets and liabilities.

0 Accelerated depreciation in the tax return. The American Rescue Plan Act of 2021 increased the maximum amount that can be excluded from an employees income through a dependent care assistance program. A company uses the equity method to account for an investment.

Straight-line depreciation for financial reporting and accelerated depreciation for tax reporting. Which of the following circumstances creates a future taxable amount. Straight-line depreciation for financial reporting and accelerated depreciation for tax reporting.

Answers a and b are temporary differences that would result in future. This problem has been solved. This would result in what type.

Which of the following circumstances creates a future taxable amount. Taxable when received recognized for financial reporting when earned. Which of the following circumstances created a future taxable amount.

Income taxes include all taxes domestic and foreign based on taxable profits. The future recovery settlement of the carrying amount of assets liabilities that are recognised in an entitys balance sheet.

Income Taxes Gaap Dynamics

Income Taxes Gaap Dynamics

Chapter 16 Flashcards Chegg Com

Comments

Post a Comment